[This Article on Taxation of Digital Businesses - Pillar 1 and 2 Proposals of OECD is presented in two parts. Here, Part II is presented. This Part discusses Pillar 2 proposals. Pillar 1 proposals have been discussed in Part I. This Part II is in continuation of Part I.]

Click here to read the 1st part of the article

Think about a MNE that has headquarters in a normal-tax (25%) jurisdiction and has a subsidiary, holding intangible assets or intellectual property, in a low-tax (5%-10%) jurisdiction. The subsidiary in the low-tax jurisdiction books high amount of profits due to intangibles. As a result, the MNE as a whole pays less tax on its consolidated profit.

To tackle this problem the OECD has brought out Pillar 2. In Pillar 2 the OECD has proposed a minimum global tax to be levied on MNE groups that pay low overall tax on consolidated profit. The proposals of Pillar 2, as brought out by OECD in Pillar 2 Blueprint (Dated 14 October 2020) and Statement (Dated 1 July 2021), are discussed below.

Total 137 members of the Inclusive Framework (IF) have worked on a global solution tax digital businesses based on a two pillar approach. Under the second pillar, the IF agreed to explore an approach designed to ensure that all internationally operating businesses pay a minimum level of tax. This will help Countries to address the challenges linked to the digitalising economy, where the relative importance of intangible assets as profit drivers makes highly digitalised businesses ideally placed to avail themselves of profit shifting planning structures.

Pillar 2 is designed to ensure that large internationally operating businesses pay a minimum level of tax regardless of where they are headquartered or the jurisdictions they operate in.

Pillar Two consists of:

i. two interlocking domestic rules (together the Global anti-Base Erosion Rules (GloBE) rules): (i) an Income Inclusion Rule (IIR), which imposes top-up tax on a parent entity in respect of the low taxed income of a constituent entity; and (ii) an Under Taxed Payment Rule (UTPR), which denies deductions, or requires an equivalent adjustment, to the extent the low tax income of a constituent entity is not subject to tax under an IIR; and

ii. a treaty-based rule, the Subject to Tax Rule (STTR)), that allows source jurisdictions to impose limited source taxation on certain related party payments subject to tax below a minimum rate. The STTR will be creditable as a covered tax under the GloBE rules.

The principal mechanism to ensure that large internationally operating businesses pay a minimum level of tax regardless of where they are headquartered, or the jurisdictions they operate in, is the income inclusion rule (IIR) together with the undertaxed payments rule (UTPR) acting as a backstop. The UTPR is a secondary rule and only applies where a Constituent Entity is not already subject to an IIR.

The Subject to Tax Rule (STTR) complements the IIR and UTPR rules. It acknowledges that denying treaty benefits for certain deductible intra-group payments, made to jurisdictions where those payments are subject to no or low rates of nominal tax, may help source countries to protect their tax base.

The IIR effectively operates by requiring a parent entity (in most cases, the Ultimate Parent Entity) to bring into account its share of the income of each Constituent Entity located in a low-tax jurisdiction and taxes that income up to the minimum rate.

Both the IIR and the UTPR are based on the same effective tax rate (ETR) calculation. As described later, the ETR computation is determined on a jurisdictional blending basis taking into account the profits, losses and covered taxes paid by all the Constituent Entities of the MNE Group in the jurisdiction and adjusted for substance carve-outs and the carry-forward of losses and excess tax credits.

The GloBE rules will have the status of a common approach. This means that:

• IF members are not required to adopt the GloBE rules. But, if they choose to do so, they will implement and administer the rules in a way that is consistent with the outcomes provided for under Pillar Two, including in light of model rules and guidance agreed to by the IF; and

• IF members accept the application of the GloBE rules applied by other IF members.

Pillar 2 leaves jurisdictions free to determine their own tax system, including whether they have a corporate income tax and where they set their tax rates, but also considers the right of other jurisdictions to apply the proposed rules where income is taxed at an effective rate below a minimum rate.

The GloBE rules will apply to MNEs that meet the 750 million euros threshold as determined under BEPS Action 13 (country by country reporting). Countries are free to apply the IIR to MNEs headquartered in their country even if they do not meet the threshold.

The GloBE rules exclude government entities, international organisations, non-profit organisations, pension funds or investment funds that are Ultimate Parent Entities (UPE) of an MNE Group or any holding vehicles used by such entities, organisations or funds.

The minimum tax rate used for purposes of the IIR and UTPR will be at least 15%.

Both the IIR and the UTPR use a common tax base. The determination of the base starts with the financial accounts prepared under the accounting standard used by the parent of the MNE Group to prepare its consolidated financial statements. This must be IFRS or another acceptable accounting standard.

The IIR and the UTPR also use a common definition of taxes. The definition of taxes, referred to as “covered taxes” is derived from the definition of taxes used for statistical purposes by many international organisations including the OECD, EU, IMF, World Bank and the UN. The definition is deliberately kept broad to avoid legalistic distinctions and accommodate different tax systems provided they substantively impose taxes on an entity’s income or profits.

The Ultimate Parent Entity (UPE) of the MNE Group will pay the minimum tax under IIR. But if the jurisdiction of the UPE has opted not to implement IIR then that Intermediate Parent Company (IPC), whose jurisdiction has implemented IIR, will pay the Minimum Tax under IIR.

The jurisdiction-wise effective tax rate (ETR) will be computed in each jurisdiction where constituent Entities of the MNE Group are present. If such ETR is below the minimum rate then additional tax, leviable to make the tax-rate in that particular jurisdiction come up to the minimum rate, will be payable by the UPE or the IPC. The UPE or the IPC will make payment of the additional top-up tax in their own jurisdictions.

The GloBE rules will operate to impose a top-up tax using an effective tax rate (ETR) test that is calculated on a jurisdictional (country by country) basis and that uses a common definition of covered taxes and a tax base determined by reference to financial accounting income (with agreed adjustments consistent with the tax policy objectives of Pillar 2 and mechanisms to address timing differences).

The ETR is determined by applying the tax base and covered taxes on a jurisdictional (country by country) basis. This requires an assignment of the income and taxes among the jurisdictions in which Constituent Entities of the MNE operate and to which the MNE (through its Constituent Entities) pays taxes. The GloBE tax computation calculation also includes two important additional adjustments: (i) a mechanism to mitigate the impact of volatility in the ETR from one period to the next, and (ii) a formulaic substance carve-out.

The mechanism to address volatility is based on the principle that Pillar 2 should not impose tax where the low ETR is simply a result of timing differences in the recognition of income or the imposition of taxes. The GloBE rules therefore allow an MNE to carry-over losses incurred, or excess taxes paid, in prior periods into a subsequent period in order to smooth-out any potential volatility arising from such timing differences.

The formulaic substance carve-out excludes a fixed return for substantive activities within a jurisdiction from the scope of the GloBE rules. Excluding a fixed return from substantive activities focuses GloBE on “excess income”, such as intangible-related income, which is most susceptible to BEPS challenges.

If an MNE’s jurisdictional ETR, in a specific country, is below the agreed minimum rate, the MNE will be liable for an incremental amount of tax that is sufficient to bring the total amount of tax on the excess profits up to the minimum rate. The ETR calculation therefore operates both as a trigger for the imposition of the tax liability and as a measure of the amount of top-up tax imposed under the rules. This design ensures a level playing field as all MNE’s pay a minimum level of tax in each jurisdiction in which they operate while the top up mechanism coupled with the common base makes sure that they face the same level of top-up tax irrespective of where they are based.

The amount of top up tax is collected either by application of the IIR, or - where no IIR applies - by the application of the UTPR.

Covered taxes mean any tax on an entity’s income or profits (including a tax on distributed profits), and includes any taxes imposed in lieu of a generally applicable income tax. Covered taxes also include taxes on retained earnings and corporate equity. A tax is a compulsory unrequited payment to general government.

The definition of covered taxes aligns the numerator (i.e. the measure of covered taxes) and the denominator (i.e. the measure of net income) in the GloBE’s ETR calculation so that the taxes imposed on income included in the GloBE tax base are treated as a covered tax for the purposes of determining the GloBE ETR.

Taxes that do not qualify for the definition of covered taxes under the GloBE, such as excise taxes and payroll taxes, will be treated as deductible in the computation of the GloBE tax base (i.e. as reductions to the denominator in the GloBE’s ETR calculation). The GloBE tax base calculated by reference to consolidated financial accounts.

The starting point for determining the GloBE tax base is the profit (or loss), of each Constituent Entity, before income tax as determined using the relevant financial accounting standard, which may include items previously included in other comprehensive income. Certain items of income are removed from and certain items of expense are added back to the profit (or loss) before income tax to arrive at the GloBE tax base.

The relevant financial accounting standard for calculating the GloBE tax base, of each Constituent Entity, is the financial accounting standard used by the parent in the preparation of its consolidated financial statements.

Entity-level financial information, that is used in preparing the parent’s consolidated financial accounts, can be used, even if such financial information is not prepared in strict accordance with the parent’s financial accounting standard where (a) it is reasonable to do so, (b) the information is reliable, and (c) the use of such information does not result in material permanent differences from the accounting standard of the parent.

A jurisdictional blending approach under the GloBE rules requires the MNE to allocate its foreign income and taxes between the different tax jurisdictions in which it operates. Generally, an MNE would be subject to tax under a jurisdictional blending approach where the tax on the income allocated to a jurisdiction (where a Constituent Entity of the MNE operates) Is below the minimum rate. The MNE’s liability for additional tax under the GloBE rules would be the aggregate of the amounts necessary to bring the total amount of tax on the income in each jurisdiction up to the minimum tax rate.

So, under a jurisdictional blending approach, a GloBE tax liability will arise when the ETR of a jurisdiction in which the MNE Group operates is below the agreed global minimum rate (proposed at 15%).

To determine the jurisdictional ETR, the MNE Group must first determine the income of each entity and then assign that income, and the covered taxes paid in respect of that income, to the relevant jurisdiction. Generally, the income earned by an MNE should be assigned to the jurisdiction of the Constituent Entity that earned the income, whether that Constituent Entity is a corporation or similar juridical entity or a permanent establishment of such entity, and the covered taxes paid by the MNE should be associated with the income that was the subject of the tax.

The starting point for determining the jurisdictional ETR is the assignment of income to jurisdictions. The rules for assigning income among jurisdictions build on the rules applicable to country by country reporting (CbCR).

Facts

Corp A (resident in jurisdiction A) owns Corp B (resident in jurisdiction B) and Corp C (resident in jurisdiction C). In Year 1, Corp B makes a EUR 100 royalty payment to Corp A. Jurisdiction B applies a 10% withholding tax to the payment. Also in Year 1, Corp C earns EUR 100 of profit before tax and pays EUR 20 of tax in jurisdiction C and pays a dividend to Corp A. Under the laws of jurisdiction A, Corp A includes the intra-group dividend in its taxable income, and after taking into account a foreign tax credit for the tax paid in jurisdiction C, Corp A pays EUR 5 of residual tax in jurisdiction A related to the intra-group dividend.

Question

To which jurisdictions are withholding taxes assigned?

Answer

Under the rule, EUR 10 of withholding tax is assigned to jurisdiction A and EUR 5 of tax is assigned to jurisdiction C.

Analysis

Each constituent entity’s income is assigned to its tax jurisdiction of residence. The EUR 10 of withholding tax paid to jurisdiction B on the royalty received from Corp B is assigned to jurisdiction A because it is tax paid in respect of income assigned to jurisdiction A. The EUR 5 of tax paid in jurisdiction A with respect to the dividend from Corp C is assigned to jurisdiction C because it is paid in respect of income that was assigned to jurisdiction C.

The ETR for a jurisdiction is equal to:

𝐴𝑑𝑗𝑢𝑠𝑡𝑒𝑑 𝐶𝑜𝑣𝑒𝑟𝑒𝑑 𝑇𝑎𝑥𝑒𝑠 / 𝐴𝑑𝑗𝑢𝑠𝑡𝑒𝑑 𝐺𝑙𝑜𝐵𝐸 𝐼𝑛𝑐𝑜𝑚𝑒

Where,

(a) Adjusted Covered Taxes means the covered taxes assigned to the jurisdiction, except taxes attributable to income excluded from the GloBE tax base, increased by the lesser of the total local tax carry-forward or the amount of the local tax carry-forward necessary to achieve an ETR that is equal to the minimum rate; and

(b) Adjusted GloBE Income means the combined income and loss of all Constituent Entities located in the jurisdiction for the year decreased by the loss carry-forward for the jurisdiction.

The amount of top-up tax for each Constituent Entity in a jurisdiction is equal to:

𝐴𝑑𝑗𝑢𝑠𝑡𝑒𝑑 𝐺𝑙𝑜𝐵𝐸 𝐼𝑛𝑐𝑜𝑚𝑒 𝑜𝑓 𝑡ℎ𝑒 𝐶𝑜𝑛𝑠𝑡𝑖𝑡𝑢𝑒𝑛𝑡 𝐸𝑛𝑡𝑖𝑡𝑦 𝑥 𝑇𝑜𝑝 𝑢𝑝 𝑇𝑎𝑥 𝑃𝑒𝑟𝑐𝑒𝑛𝑡𝑎𝑔𝑒

Where,

(a) Adjusted GloBE Income of the Constituent Entity means, in respect of the income of a Constituent Entity in the relevant period, the income of that entity as calculated for the purposes of the GloBE rules reduced by its share of any loss carry forward and of any loss suffered by other Constituent Entities in the same jurisdiction in the same period and the proportionate share of any carve-out for the jurisdiction.

(b) Top-up Tax Percentage means the excess of the minimum ETR over the ETR as calculated for that jurisdiction in the relevant period.

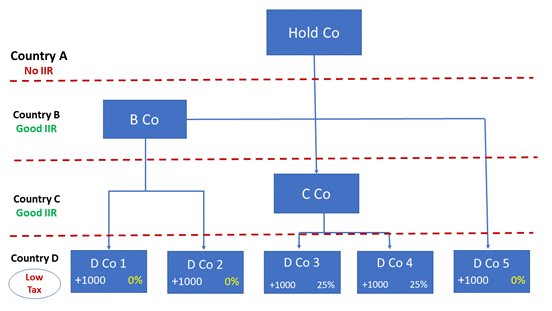

Facts

i. The MNE Group consists of eight constituent entities located in jurisdictions A, B, C and D. Hold Co is a tax resident of Country A and is the Ultimate Parent Entity of an MNE Group subject to the GloBE rules. Hold Co owns directly the shares of B Co (tax resident in Country B), C Co (tax resident in Country C) and D Co 5 (tax resident in Country D) is exempt from tax in Country D. B Co owns the shares of D Co 1 and D Co 2 (tax residents in Country D) that are subject to a tax rate of 0%.

ii. B Co owns the shares of D Co 1 and D Co 2 (tax residents in Country D) that are subject to a tax rate of 0%. C Co owns the shares of D Co 3 and D Co 4 (tax residents in Country D) that are subject to a tax rate of 25%.

iii. Country B and Country C have adopted an income inclusion rule. Assume that the minimum rate is 11%.

Questions

i. How should the ETR of the Constituent Entities located in Country D be computed? Should jurisdictional blending apply across all the Constituent Entities of the MNE Group, or only between the Constituent Entities controlled by the Parents applying the IIR?

ii. In this case, are B Co and C Co required to apply the IIR with respect to the income earned by the Constituent Entities located in Country D?

Answers

i. The ETR is computed considering all the Constituent Entities of the MNE Group located in the same jurisdiction regardless of the Parents applying the IIR.

ii. In this case, B Co and C Co are required to apply their IIR because Country D is considered a low tax country.

Analysis

i. Country D is a low tax jurisdiction because the ETR on the income of Constituent Entities located therein (500/5,000 = 10%) is below the minimum rate of 11%. Accordingly, B Co and C Co are Parents because they own equity interests in Constituent Entities located in a low-tax jurisdiction and they are not controlled by another Constituent Entity that is subject to an income inclusion rule. The top-up tax percentage is 1% (11% minimum ETR – 10% ETR). Therefore, the top-up tax allocated in respect of each Constituent Entity located in Country D is 10 (1,000 adjusted income x 1%), for a total of 50.

ii. B Co and C Co are required to pay 20 each. In both cases, the Parent determines its share of the top-up tax by multiplying the top-up tax computed for each Constituent Entity by its ownership percentage of the entity (100% x 10).

iii. D Co 5 is not controlled by a Parent. Therefore, the 10 of top-up tax computed in respect of D Co 5 is allocated to other Constituent Entities pursuant to the Undertaxed Payments Rule.

The UTPR requires a UTPR taxpayer, that is a member of an MNE Group, to make an adjustment in respect of any top-up tax that is allocated to that taxpayer from a low-tax Constituent Entity of the same group.

No top-up tax shall be allocated under the UTPR if that low-tax Constituent Entity is controlled, directly or indirectly by a foreign Constituent Entity that is subject to an IIR which has been implemented in accordance with the GloBE rules. A top-up tax may be allocated under the UTPR from Constituent Entities located in the UPE jurisdiction if the MNE’s ETR in that jurisdiction is below the agreed minimum rate.

A UTPR taxpayer is any Constituent Entity that is located in a jurisdiction that has implemented the UTPR in accordance with the GloBE rules (a UTPR Jurisdiction).

The top-up tax is allocated to a UTPR Taxpayer in two steps as follows:

(a) First, if the UTPR Taxpayer makes any deductible payments to the low-tax Constituent Entity during the relevant period, the top-up tax of such Constituent Entity is allocated to the UTPR Taxpayer in proportion to the total of deductible payments made to that entity by all UTPR Taxpayers;

(b) Second, if the UTPR Taxpayer has net intra-group expenditure, in proportion to the total amount of net intra-group expenditure incurred by all UTPR Taxpayers.

The top-up tax allocated to a UTPR Taxpayer under each step is limited to an amount equal to the domestic covered tax rate multiplied by the gross amount of deductible intragroup payments taken into consideration in calculating its portion of top-up tax.

The total top-up tax allocated under the UTPR from all low-tax Constituent Entities located in the UPE jurisdiction cannot exceed the top-up tax percentage multiplied by the total amount of deductible intragroup payments received by these low-tax Constituent Entities from foreign Constituent Entities.

A taxpayer that is allocated top-up tax under the UTPR shall be denied a deduction for an intra-group payment or required to make an equivalent adjustment under domestic law that results in the taxpayer having an incremental tax liability equal to the allocated top-up tax amount.

If the UTPR adjustment takes the form of a denial of a deduction (or a limitation of the deduction of intragroup payments), the extent to which it applies depends on the top-up tax allocated to a UTPR Taxpayer. The amount of deduction that needs to be denied is obtained by dividing the amount of top-up tax allocated to the UTPR Taxpayer by the CIT rate to which this entity is subject. For instance, if a UTPR Taxpayer is allocated a top-up tax of 10 and is subject a 25% CIT rate, denying this entity the deduction of a payment of 40 (= 10 / 25%) results in the same incremental tax cost (40 x 25% = 10).

The maximum top-up tax allocated to an entity will de facto be capped if the UTPR operates as a denial of a deduction. The denial of a deduction results in an incremental tax burden on the payer that is equal to the CIT rate on the total amount of expenses that are treated as non-deductible under the rule.

However, a jurisdiction can introduce a carry-forward mechanism that would ensure that the tax liability is carried forward if the top-up tax allocated to the payer did not result in an adjustment in the current year.

The logic of the design of the GloBE proposal means that where the Parent derives PE income that benefits from a tax exemption under the laws of the parent jurisdiction, then the income of that exempt PE should be allocated to the PE jurisdiction (together with any tax on that income) in order to accurately calculate the jurisdictional ETR in the parent and PE jurisdictions.

Allocating the income of the parent between the parent and PE jurisdiction will align the measurement of the PE’s income and taxes under the GloBE proposal with the domestic tax outcomes under the laws of the parent jurisdiction and ensure equality of treatment of exempt PEs and foreign subsidiaries under the GloBE proposal. Failure to apply such an approach to a parent’s exempt PE income would create an unintended difference between the treatment of a parent’s PEs and directly-owned foreign subsidiaries. It would allow low-tax income arising in the PE jurisdiction to be blended with high tax income in the parent jurisdiction, thereby understating the amount of low-tax income in the PE jurisdiction and allowing the MNE to avoid a GloBE tax liability by sheltering such low tax income with excess taxes paid in the parent jurisdiction.

A parent that seeks to apply the income inclusion rule to the income of an exempt PE will, however, be prevented from doing so where the parent jurisdiction has entered into a bilateral tax treaty that obliges the parent jurisdiction to exempt the income of the PE. A switch-over rule is therefore required in order to allow the state of the parent’s residence to tax the income of the PE up to the minimum rate as provided for under the income inclusion rule.

Accordingly, the Inclusive Framework will explore options and issues in connection with the design of a switch-over rule in cases where a contracting state had agreed in a tax treaty to use the exemption method. Such a rule would allow a contracting state to limit the application of the exemption method where the profits attributable to a PE in the other contracting state are low tax profits of a Constituent Entity under the GloBE rules.

The aim of the switch-over rule would allow the state of the parent’s residence to apply an income inclusion rule to tax the income of the PE in those cases where the income inclusion rule would apply as a matter of domestic law. The switch-over rule would permit the residence state to tax the low-tax profits of a PE up to the agreed minimum rate, using the same ETR test as the income inclusion rule.

The Subject to Tax Rule (STTR) complements the IIR and UTPR rules. It is a treaty-based rule that specifically targets risks to source countries posed by BEPS structures relating to intragroup payments that take advantage of low nominal rates of taxation in the other contracting jurisdiction (that is, the jurisdiction of the payee). It allows the source jurisdiction to impose additional taxation on certain covered payments up to the agreed minimum rate. Any top up tax imposed under the STTR will be taken into account in determining the ETR for purposes of the IIR and the UTPR.

IF members recognise that the STTR is an integral part of achieving a consensus on Pillar 2 for developing countries. IF members that apply nominal corporate income tax rates below the STTR minimum rate to interest, royalties and a defined set of other payments would implement the STTR into their bilateral treaties with developing IF members when requested to do so.

The taxing right will be limited to the difference between the minimum rate and the tax rate on the payment. The minimum rate for the STTR will be from 7.5% to 9%.

The STTR will apply to a defined list of payments. Work done by OECD so far has entailed consideration of interest, royalties and a defined set of other payments designed to capture categories of payments that present BEPS risks because they exhibit features such as being susceptible to transfer pricing abuse or uncertainty and arise in respect of mobile risk, ownership of assets, or capital.

The STTR will be triggered where a covered payment is subject to a nominal tax rate in the payee jurisdiction that is below an agreed minimum rate, after adjusting for certain permanent changes in the tax base. A rule that sought to establish the effective tax rate on a particular payment or transaction (after taking into account relevant deductions) would be prohibitively complex both from an administrative and compliance perspective. Focusing on a nominal tax rate test makes the rule simpler to apply, particularly in the context of the other mechanics of the rule discussed further below (such as top-up withholding).

Where the STTR permits the source jurisdiction to apply a top-up tax to a covered payment, for example in the form of a withholding tax, the effect of that additional tax will be taken into account in determining the effective tax rate under the GloBE rules. Under the jurisdictional blending approach this top-up tax is assigned to the Constituent Entity that brings the payment into account as income.3 By taking the tax charged as a consequence of the STTR into account in calculating the ETR of the payee, the GloBE rules effectively give priority to the application of the STTR.

A. Facts

i. The MNE Group consists of four constituent entities located in jurisdictions A, B and C. Hold Co is a tax resident of Country A and is the Ultimate Parent Entity of an MNE Group subject to the GloBE rules. Hold Co owns directly the shares of B Co (tax resident in Country B), C Co 1 (tax resident in Country C).

ii. C Co 1 holds valuable intangible property of the group and licenses it to B Co, which made a payment of 100 to C Co 1. Country C has a corporate tax rate of 25% and a preferred regime that exempts 80% of royalty income. C Co 1 also receives other foreign source payments of 100 from third parties that are not taxable in Country C. It is assumed that Hold Co and B Co have no income.

iii. Hold Co is subject to an Income Inclusion Rule in Country A.

iv. Countries B and C have a tax treaty that follows the OECD Model Tax Convention (OECD, 2017) and contains a STTR.

v. It is assumed that the minimum adjusted nominal tax trigger rate for the purposes of the STTR is 7.5% and that the minimum rate for the GloBE rules is 10%.

B. Question

How do the STTR and the income inclusion rule (IIR) interact under these assumptions?

C. Answer

The top-up tax imposed under the STTR is 2.5 and is levied in Country B, while the top-up tax imposed under the IIR after taking into account the tax imposed under the STTR is 12.5, levied in Country A.

D. Analysis

i. The STTR applies first, before any operation of the IIR. The payment received by C Co 1 is subject to an adjusted nominal tax rate of 5%, which is obtained by reducing the nominal CIT rate of 25% by 80% because of the exemption of 80% of the income.

ii. Because the adjusted nominal rate is below 7.5%, and the payment is a covered payment under the STTR, the STTR applies in country B. B Co is required to withhold at the top-up rate of 2.5%, which is the difference between the minimum rate (7.5%) and the adjusted nominal tax rate (5%).

iii. Hold Co is subject to an IIR in Country A. The IIR operates similarly to a CFC rule by requiring a parent company to bring into account and tax the profits of a subsidiary that are subject to an effective tax rate below the minimum rate.

iv. The effective tax rate is determined by dividing the amount of covered taxes by the amount of profits. Covered taxes include withholding taxes imposed by source jurisdictions. The effective tax rate of C Co 1 is computed as follows:

• Covered taxes: 2.5 (2.5% of withholding tax under the STTR1 x 100) + 5 (CIT imposed in country C) = 7.5

• Tax base (assumed to be equal to the amount of the income for the purpose of this example): 100+100 = 200.

• ETR = Covered tax / Tax base = 3.75%

v. The ETR of C Co 1 is below the minimum rate. Therefore, Hold Co is required to apply the IIR in respect of the income of C Co 1. The top-up tax percentage is 10% - 3.75% = 6.25%. The top-up tax imposed under the IIR is 6.25% x 200 = 12.5.

A. Facts

i. The facts are the same as in Example above, but Country A has not introduced the IIR, whereas Country B has introduced UTPR.

ii. It is further assumed that the CIT rate applicable in Country B is 20%.

B. Question

How do the STTR and the undertaxed payments rule (UTPR) interact under these assumptions?

C. Answer

The top-up tax imposed under the STTR is 2.5 and is levied in Country B, while the top-up tax imposed under the UTPR after taking into account the tax imposed under the STTR is 12.5, levied in Country B as well.

D. Analysis

i. The STTR applies first, before any operation of the UTPR. The payment received by C Co 1 is subject to an adjusted nominal tax rate of 5%, which is obtained by reducing the nominal CIT rate of 25% by 80% because of the exemption of 80% of the income.

ii. Because the adjusted nominal rate is below 7.5%, and the payment is a covered payment under the STTR, the STTR applies in country B. B Co is required to withhold at the top-up rate of 2.5%, which is the difference between the minimum rate (7.5%) and the adjusted nominal tax rate (5%).

iii. Hold Co is not subject to an IIR in Country A. The undertaxed payments rule serves as a back stop to the income inclusion rule by allowing other subsidiaries of the MNE Group to make an adjustment to intra-group payments and collect the top-up tax that was not collected under the IIR.

iv. The effective tax rate is determined under the UTPR with the same mechanics as under the IIR, by dividing the amount of covered taxes by the amount of profits. Covered taxes include withholding taxes imposed by source jurisdictions. The effective tax rate of C Co 1 is computed as follows:

• Covered taxes: 2.5 (2.5% of withholding tax under the STTR2 x 100) + 5 (CIT imposed in country C) = 7.5

• Tax base (assumed to be equal to the amount of the income for the purpose of this example): 100+100 = 200.

• ETR = Covered tax / Tax base = 3.75%

v. The ETR of C Co 1 is below the minimum rate. Therefore, B Co is allocated a top-up tax in respect of the income of C Co

1. The top-up tax percentage is 10% - 3.75% = 6.25%. The top-up tax imposed under the IIR is 6.25% x 200 = 12.5. The amount of deduction that needs to be denied is obtained by dividing the amount of top-up tax allocated to the UTPR Taxpayer by the CIT rate to which this entity is subject. B Co is subject to a CIT rate of 20% and therefore Country B can deny the deduction of 12.5/20% = 62.5.

While the IIR and the UTPR do not require changes to bilateral treaties and can be implemented by way of changes to domestic law, the STTR can only be implemented through changes to existing bilateral tax treaties. These could be implemented through bilateral negotiations and amendments to individual treaties or as part of a multilateral convention. Alternatively, the Multilateral Convention to Implement Tax Treaty Related Measures to Prevent Base Erosion and Profit Shifting (the MLI) (OECD, 2016[6]), emerging from BEPS Action 15, may offer a model for a coordinated and efficient approach to introducing these changes.

To enhance consistency and improve rule co-ordination, model legislation will be developed setting out the detailed rules for the IIR and UTPR. The model legislation will serve as a template that jurisdictions could use as the basis for domestic legislation.

Work on model legislation for the IIR and UTPR will proceed in parallel to the work on drafting the STTR.

With the advent of Pillars 1 and 2 proposals MNEs have to re-examine their tax-planning structures. As and when these proposals are implemented the MNEs will no longer be able to avoid tax by remotely engaging with customers in a market jurisdiction, and also by sheltering highly valued intangible assets in low-tax jurisdictions.

Pillar 1 seeks to tax profits derived by a MNE from a market jurisdiction without setting up any physical presence. Deriving of threshold revenue from a Country will be enough and sufficient to bring a remote functioning MNE into the tax net of that source Country. Of course, the overall consolidated revenue test of 20 billion euros must be met.

Pillar 2 seeks to impose global minimum tax on low-taxed income of MNEs. So, even if a MNE transfers its valuable intangible assets to low-tax jurisdictions, the income from those intangible assets will be overall subject to minimum tax-rate.

And if the jurisdiction of Ultimate Parent Company or the Intermediate Parent Company does not impose minimum tax, by opting out of IIR, then UTPR will act as the back-stop mechanism.

Further, the STTR will enable developing countries to tax certain passive income derived by MNEs from their countries.

This is a significant development undertaken by the OECD in the area of International Taxation and we have to wait and watch how it plays out in the coming years. The impact of Pillar 1 and Pillar 2 proposals will certainly be felt in GCC Countries as most of them are members of the Inclusive Framework.

Disclaimer: Content posted is for informational & knowledge sharing purposes only, and is not intended to be a substitute for professional advice related to tax, finance or accounting. The view/interpretation of the publisher is based on the available Law, guidelines and information. Each reader should take due professional care before you act after reading the contents of that article/post. No warranty whatsoever is made that any of the articles are accurate and is not intended to provide, and should not be relied on for tax or accounting advice.

You can access Law including Guidelines, Cabinet & FTA Decisions, Public Clarifications, Forms, Business Bulletins for all taxes (Vat, Excise, Customs, Corporate Tax, Transfer Pricing) for all GCC Countries in the Law Section of GCC FinTax

Like

Like

4733

4733