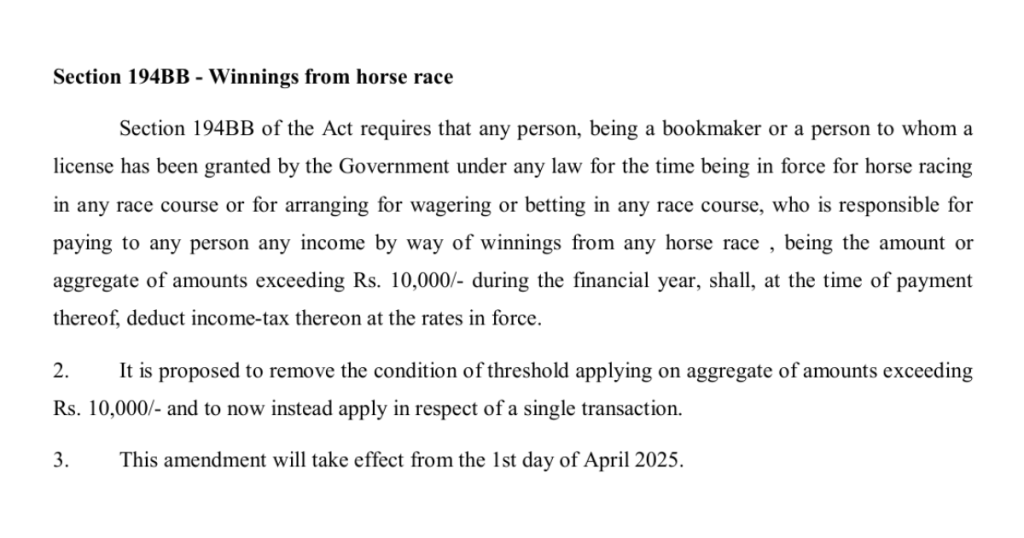

As per section 194BB of the Income Tax Act of 1961, Winnings from horse race―

Any person, being a bookmaker or a person to whom a license has been granted by the Government under any law for the time being in force for horse racing in any race course or for arranging for wagering or betting in any race course, who is responsible for paying to any person any income by way of winnings from any horse race in an amount exceeding ten thousand rupees shall, at the time of payment thereof, deduct income-tax thereon at the rates in force.

Starting April 1, 2025, there will be substantial modifications to the Tax Deducted at Source (TDS) on horse racing winnings as outlined in Section 194BB of the Income Tax Act.

As Per The Finance Bill, 2025

The amendments are designed to streamline compliance for both prize distributors and winners, minimizing confusion related to cumulative calculations of winnings over the financial year.

New Threshold for TDS

The most significant change is eliminating the aggregate threshold limit of ₹10,000.

Previously, TDS applied when the total winnings from a single-payer exceeded this amount within the financial year.

According to the new regulations, TDS will now be deducted only if an individual transaction surpasses ₹10,000.

TDS Rate

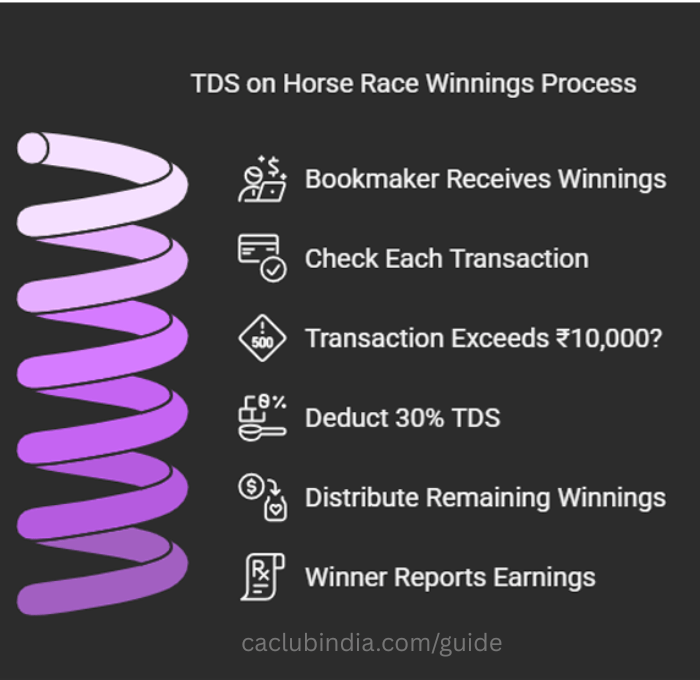

The TDS rate remains at 30% on winnings from horse races, with no additional surcharges or cess applicable. This rate will be applied at the time of payment to the winner.

Applicability

The obligation to deduct TDS falls on bookmakers or licensed entities engaged in horse racing and wagering activities. They must withhold tax prior to distributing winnings that surpass the specified threshold.

Implications For Winners

Winners are required to report their earnings in their income tax returns, even if TDS is not deducted because the winnings are below ₹10,000.

Example

| Winnings: ₹15,000 TDS Deduction TDS Rate: 30% TDS Amount: ₹15,000 × 30% = ₹4,500 Amount Received After TDS deduction: ₹15,000 – ₹4,500 = ₹10,500 |

The winner must report the full ₹15,000 as income in their tax return and will receive a credit for the ₹4,500 TDS deducted. This amount can be adjusted against their total tax liability.

These changes signify a broader shift in tax regulations, focused on improving transparency and streamlining tax collection from gambling and betting activities.

How will the removal of the aggregate threshold limit affect prize distributors?

- Individual Transaction Reporting

- Immediate Compliance

- Administrative Efficiency

- Reduced Complexity

- Cash Flow Considerations

- Immediate Tax Deductions

Penalties For Non-Compliance

- Interest Penalty – If an entity fails to deduct TDS or does not deposit the deducted TDS within the stipulated time, interest will be charged at the rate of 1% per month for the period of delay in deducting and 1.5% per month for the period of delay in depositing TDS.

- Late Filing Fee under Section 234E – If TDS returns are filed late, a fee of ₹200 per day is applicable until the failure is rectified. However, the total fee cannot exceed the amount of TDS that should have been deducted or paid.

- General Penalty under Section 271C – A penalty can be imposed under this section if a person fails to deduct TDS. The penalty can be equal to the amount of tax that should have been deducted.

- Penalty Under Section 276B – If a taxpayer fails to pay the TDS after deduction, they can face imprisonment for a term ranging from 3 months to 7 years and can also attract a fine.

Exemptions To The TDS Rules u/s 194BB

- TDS under Section 194BB is only applicable if the income exceeds a certain amount. If the total income from the specified games is below ₹10,000 in a financial year, TDS is not applicable.

- If the income is earned by a non-resident player, TDS provisions may differ, and tax liability may be determined based on the provisions related to non residents. Generally, non-residents may be subject to different tax rates under relevant Double Taxation Avoidance Agreements (DTAA).

- TDS does not apply unless the income has been explicitly assessed as income under the Income Tax Act. If a player does not meet the criteria for being subjected to income tax on winnings from such games, TDS may not be applicable.

- Regular participants in horse races who expect substantial winnings can apply for an exemption certificate under Section 197. This certificate allows them to receive their winnings without any TDS deduction, provided it is valid for a specific period and must be renewed before expiration

FAQs

- What is the new TDS rule u/s 194BB?

Currently, TDS is deducted on winnings from horse races if the total winnings exceed ₹10,000 in a financial year.

But starting from 1st April 2025, TDS will be applied on each individual transaction exceeding ₹10,000. - Who is liable to deduct TDS under Section 194BB?

Bookmakers and licensed racecourse operators must deduct TDS before making payments.

- How will this amendment impact winners?

Winners will now face TDS deduction on every winning transaction exceeding ₹10,000, rather than the cumulative winnings over a financial year.