As per Section 271C of the Income Tax Act 1961, states that the “Penalty for failure to deduct tax at source”-

(1) If any person fails to—

(a) deduct the whole or any part of the tax as required by or under the provisions of Chapter XVII-B; or

(b) pay the whole or any part of the tax as required by or under-

(i) sub-section (2) of section 115-O; or

(ii) the second proviso to section 194B,

then, such person shall be liable to pay, by way of penalty, a sum equal to the amount of tax which such person failed to deduct or pay as aforesaid.]

(2) Any penalty imposable under sub-section (1) shall be imposed by the Joint Commissioner.

In short, Section 271C of the Income Tax Act of 1961, pertains to penalties imposed for not deducting tax at source (TDS) or for failing to remit the TDS to the government. This section is vital in promoting adherence to tax responsibilities and deterring tax evasion.

Key Provisions of Section 271C

Penalty for Non-Deduction

If an individual or entity does not deduct the full amount or any portion of the tax required under Chapter XVII-B of the Act, they may face a penalty. This penalty could amount to the entire Tax Deducted at Source (TDS) that should have been withheld but was not.

Failure to Remit TDS

If an individual or entity does not deduct the full amount or any portion of the tax required under Chapter XVII-B of the Act, they may face a penalty. This penalty could amount to the entire Tax Deducted at Source (TDS) that should have been withheld but was not.

Specific Situations

The penalties under Section 271C can be imposed in various circumstances, including:

- Failure to deduct TDS on salary payments (Section 192)

- Non-deduction of TDS on professional fees (Section 194J)

- Non-compliance with TDS on contractor payments (Section 194C)

| Default Situation | TDS Deduction Required | Penalty Applied |

| Failure to deduct TDS on salary payments | Section 192 (Salary) | Penalty of TDS amount |

| Failure to deduct TDS on professional fees | Section 194J (Professional Fees) | Penalty of TDS amount |

| Failure to deduct TDS on contractor payment | Section 194C (Contractor Payment) | Penalty of TDS amount |

| Failure to remit deducted TDS timely | All Sections | Penalty equivalent to unpaid TDS |

| Failure to pay deducted TDS | All Sections | Penalty of TDS amount |

As Per The Memorandum Of The Finance Bill, 2025 – The Current Amendment

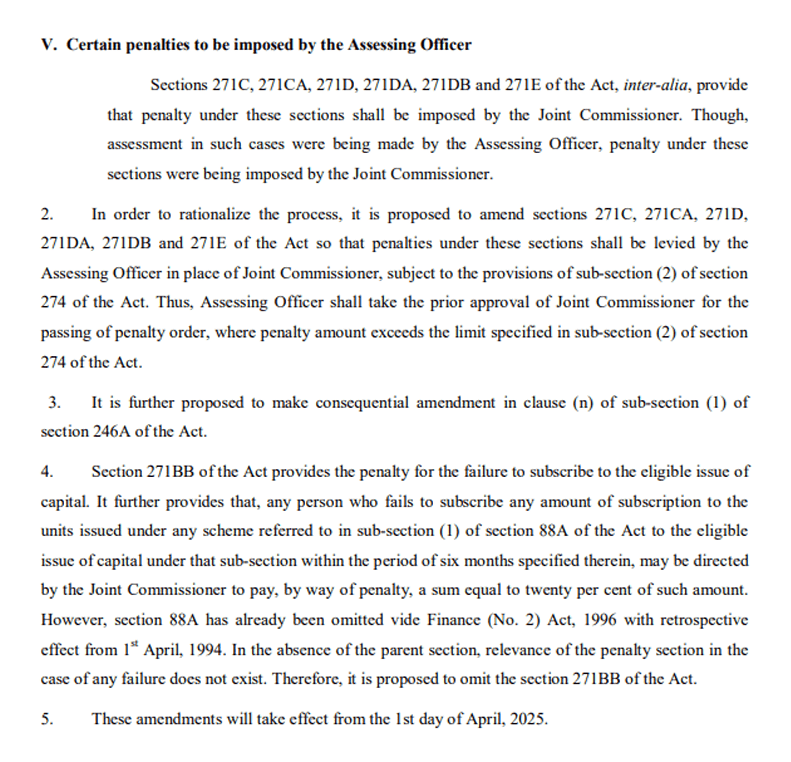

Starting April 1, 2025, the responsibility for imposing penalties under Section 271C (failure to deduct TDS) of the Income Tax Act will be transferred from the Joint Commissioner to the Assessing Officer (AO). This change, part of the Finance Bill, 2025, will also impact Sections 271CA (failure to furnish TDS returns), 271D (acceptance of loans or deposits in cash), 271DA (failure to report cash transactions), 271DB (failure to comply with the reporting requirements), and 271E (repayment of loans or deposits in cash), simplifying the penalty process by consolidating assessment and penalty authority under the AO.

As per the changes outlined in the Finance Bill, 2025, there is a significant modification concerning the authority to impose penalties under Section 271C of the Income Tax Act. Here are the key aspects of this provision:

- The change introduced in the Finance Bill, 2025, regarding the authority to impose penalties under various sections of the Income Tax Act marks a significant shift in the administration of tax penalties in India.

- By consolidating assessment and penalty imposition under the AO’s purview, the process is likely to be simplified. This could lead to more efficient handling of cases, as the same officer will assess and determine penalties.

- With the AO taking on the responsibility for imposing penalties, there may be a greater emphasis on accountability and consistency in decision-making. The AO will likely have a better understanding of the particulars of each case they encounter.

- The shift is likely to streamline the penalty imposition process, making it more efficient by allowing AOs, who are directly involved in the assessment of taxpayers, to handle penalty decisions themselves.

- AOs will have a better understanding of individual cases due to their ongoing responsibilities related to taxpayer assessments.

FAQs

- What are the main reasons behind the shift in penalty imposition from Joint Commissioner to Assessing Officer?

Streamlining Penalty Procedures, Decentralization of Authority, Improved Enforcement, Avoidance of Mechanical Approvals, Simplification of Legal Timelines.

- What are the potential challenges for Assessing Officers with this new authority?

Complexity of Tax Provisions, Resource Constraints, Balancing Efficiency and Fairness, Handling Complex Disputes, Technological Adaptation, Arbitrary Case Allotment,

Cybersecurity Concerns, Judicial Oversight Issues, - Can penalties be imposed without Joint Commissioner approval?

AOs can impose penalties up to Rs 10,000 or Rs 20,000 (depending on the designation of the officer) without requiring prior approval from the Joint Commissioner. However, if the penalties exceed these amounts, obtaining that approval is necessary.