TDS (Tax Deducted at Source) is a mechanism in which tax is deducted during specific payments, including salaries, rent, professional fees, interest, and contract payments. The deductor (the one making the payment) retains a designated tax percentage before disbursing the payment to the deductee (the recipient) and then submits this amount to the government.

TCS is a mechanism in which the seller collects tax from the buyer at the point of sale for certain specified goods and services. The seller then remits the collected tax to the government.

The Indian Budget for 2025 has announced important modifications to the TDS (Tax Deducted at Source) and TCS (Tax Collected at Source) regulations, especially in relation to individuals who do not file income tax returns. These updates will be implemented starting April 1, 2025.

Key Changes

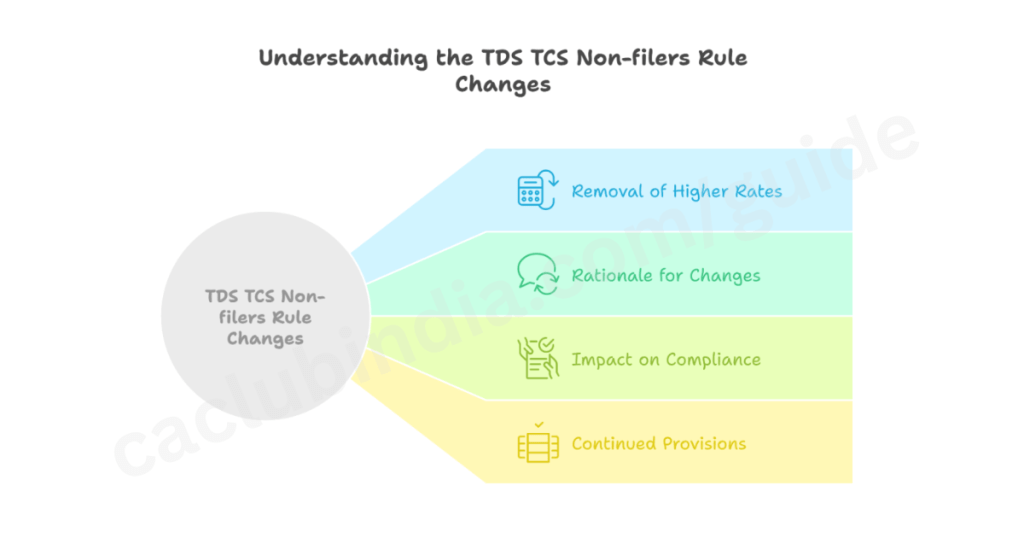

Removal of Higher Rates

The budget has eliminated the provisions outlined in Sections 206AB and 206CCA of the Income Tax Act, which imposed elevated TDS and TCS rates on individuals who had not filed their income tax returns. Under these sections, deductors were required to apply a TDS rate that was either double the standard rate (or 5%, whichever was greater) for non-filers, with analogous rules concerning TCS.

Section 206AB

Mandated that TDS (Tax Deducted at Source) be deducted at a higher rate for individuals and entities who had not filed their income tax returns for the preceding financial year. The rate was set at twice the prescribed TDS rate or 5%, whichever was higher, incentivizing compliance through financial penalties.

Section 206CCA

Set similar provisions for TCS (Tax Collected at Source), requiring higher TCS rates for non-filers.

These provisions were introduced to encourage compliance among taxpayers, increasing the filing of income tax returns by imposing financial disincentives on those who failed to file.

Rationale for Changes

The implementation of these sections in the Union Budget 2021 was intended to promote the prompt filing of income tax returns. Nonetheless, they unintentionally heightened the compliance challenges for businesses and financial institutions, complicating their ability to verify the filing status of deductees and collectees. Stakeholders raised concerns about the operational difficulties and potential errors that could result from these new requirements.

Businesses and financial institutions faced challenges in verifying the filing status of each deductee or collectee. The requirement to check the compliance status created an additional operational step that was not present before.

Impact on Compliance

By eliminating these higher rates, the government seeks to streamline tax compliance and ease administrative burdens for deductors and collectors, particularly aiding small businesses and individuals who struggled under these regulations. This decision underscores a broader commitment to creating a taxpayer-friendly environment and improving the ease of doing business in India.

With the elimination of higher rates, the compliance process becomes less complex. Deductors and collectors can focus on their core operations without being bogged down by the intricacies of verifying compliance statuses.

Small businesses, which often operate with limited resources, stand to benefit the most. They can redirect their attention and resources to growth and operational efficiency instead of extensive compliance checks and potential penalties.

Continued Provisions

It’s crucial to emphasize that although the higher rates for non-filers will be eliminated, the current rules concerning elevated TDS/TCS rates for cases with invalid or absent Permanent Account Numbers (PAN) will remain in effect.

The existence of these provisions serves as an encouragement for taxpayers to ensure their PAN details are accurate and up to date. This can help avoid unintended higher tax deductions and fosters better compliance with tax regulations.

Businesses must ensure proper documentation and verification of PANs when transacting with clients, suppliers, or employees.

Conclusion

Eliminating these provisions is an important advancement in easing compliance responsibilities and fostering a more streamlined operational environment for taxpayers in India.

These adjustments reflect the government’s dedication to simplifying tax processes and cultivating a friendly atmosphere for taxpayers.

The abolition of elevated TDS/TCS rates for non-filers, along with the decriminalization of late TCS payments, represents a substantial move towards lowering the compliance burden and enhancing the ease of doing business in India.