I am in TamilnaduITC SETOFFV Rules w.e.f ? and another one

we have an Igst credit note that is adjustable in Cgst or carry the Next month

Menu

Forum Search

Rule ITC setoff 88A

Replies (17)

Mr. Lingam,

Please elaborate the concern.

On 02 August 2019 at 10:09

Dharma Lingam

72 Points

Posted on 02 August 2019

inputCgst& Sgst =50000& igst =280000

output chat&sgst=90000&igst190000

Credit Note in igst = 62000

explain this

output chat&sgst=90000&igst190000

Credit Note in igst = 62000

explain this

On 02 August 2019 at 10:19

Credit Note for Sales Return?

On 02 August 2019 at 10:27

Dharma Lingam

72 Points

Posted on 02 August 2019

sorry that is an Debiite note I have mentioned in party Invoice

On 02 August 2019 at 10:30

Means you have returned the Goods to the seller?

On 02 August 2019 at 10:40

Mr. Lingam,

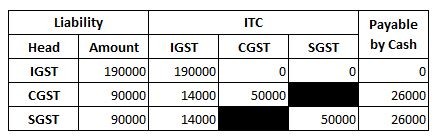

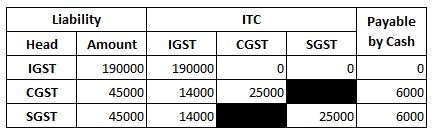

Then your Input of IGST would get reduced by 62000.

Input of CGST/SGST=50000 & IGST=218000 (i.e. 280000 - 62000)

Output of CGST/SGST=90000 & IGST=190000

Output of IGST 190000 would get set off with Input of IGST 190000 (Input IGST of 28000 would remain)

Output of CGST/SGST 90000 would get set off with Input of IGST 28000 (in any order or proportion) say, 14000 each.

Output of remianing CGST/SGST i.e. 62000 would get set off with Input of CGST/SGST 50000 say, 25000 each.

Output of remaining CGST/SGST i.e. 12000 needs to be paid in Cash say, 6000 each.

Set Off can be made in below mentioned order:

First, ITC of IGST needs to be used to set off IGST Liability.

Second, ITC of IGST needs to be used to set off CGST or SGST Liability, in any order or proportion. Make sure that ITC of IGST is exhausted before moving ahead.

Third, ITC of CGST or SGST can be used to set off other liability as applicable in below mentioned order.

ITC of CGST with CGST then IGST

ITC of SGST with SGST then IGST

You can refer to the below link for more details.

https://www.cbic.gov.in/htdocs-cbec/gst/Circular-98-17-2019-GST.pdf

On 02 August 2019 at 10:51

Dharma Lingam

72 Points

Posted on 02 August 2019

I can't understand actually Igst Excess 28000/- it's dived to chat& sgst 14000 but y have reduced Each 28000/-

On 02 August 2019 at 11:44

Input of CGST/SGST=50000 & IGST=218000 (i.e. 280000 - 62000) Output of CGST/SGST=90000 & IGST=190000

Is CGST/SGST mentioned here is for both or each?

On 02 August 2019 at 11:48

If it is for each:

If it is for both:

On 02 August 2019 at 11:58

Dharma Lingam

72 Points

Posted on 02 August 2019

I thing y said 52000 we have to paid amount on this month

On 02 August 2019 at 12:25

Yes, as you dont have that much of ITC available with you

On 02 August 2019 at 13:36

Dharma Lingam

72 Points

Posted on 02 August 2019

Somebody said first set-off the igst after cgst then will clear the sgst but as per formula excess amount will be divided in cgst & sgst which one is correct? pls clarify that and also need to know Wef. date in Tamilnadu

On 02 August 2019 at 13:38

Please share your way of setting off.

On 02 August 2019 at 14:01

Leave a Reply

Your are not logged in . Please login to post replies

Click here to Login / Register

Recent Topics :

- GST ITC april 22

- GST PAYMENT REGARDING

- GST Consultation Required – June–Augus

- TDS Code for Salary Payment to Non-Resident Intern

- TDS on property

- Company data for software

- Car purchase to be eligible for ITC

- GST Refund on payment to builder

- TDS u/s 194Q on electricity supply by DHBVN etc.

- Subject: Can I Apply for Fresh GST Registration on

Related Topics :

CAclubindia

CAclubindia