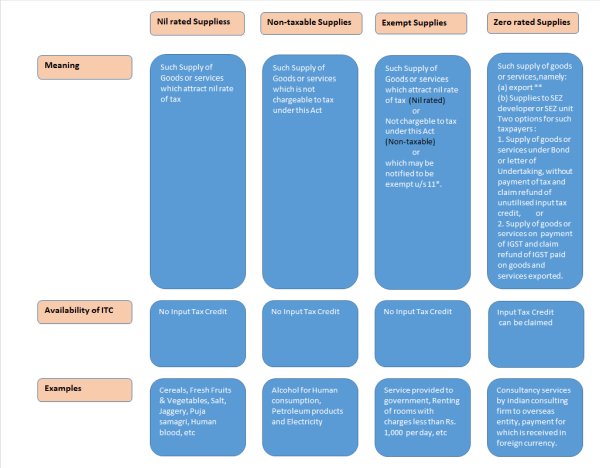

Nil Rated, Zero Rated, Non-taxable and Exempt Supplies

With the Introduction of Goods and service Tax(GST), the traders are left confused with some of the provisions of the Act. Taking into consideration one such tangled provision, as to what is the difference between Nil rated and zero rated supplies, as well as non-taxable and exempt supplies.

While the end result of all these supplies is the same, i.e. GST is not charged on the supply. But, from the reporting point of view, a clear bifurcation is required to be furnished in the GST Returns.

Schedule to GST law prescribe the rate of GST for supply of goods and services. These rates are fixed by the parliament and changing these rates is time consuming.

However, Government needs flexibility in operating of taxing statute. As the circumstances change, quick adoption to changing situation is required.

* Hence, As per section 11(1), of CGST and SGST Act, Central/State government has been granted the power to reduce GST rates as per requirements, by issuing a general exemption notification. The notification can be issued only on the basis of recommendation of the GST council. The exemption should be in public interest.

The general exemption can be general either absolutely or subject to such conditions as may be specified in the notification. The exemption can be absolute (unconditional) or subject to conditions. The exemption can be in respect of goods or services or both of any specified descripttion. Exemption can be from the whole or any part of the tax leviable thereon.

There is identical provision in section 6(1) of IGST Act.

** Export of Goods or Services

"Export of goods" means taking goods out of India to a place outside India.

"Export of services" means the supply of any service when:

(a) the supplier of service is located in India,

(b) the recipient of service is located outside India,

(c) the place of supply of service is outside India,

(d) the payment for such service has been received by the supplier of service in convertible foreign exchange, and

(e) the supplier of service and recipient of service are not merely establishments of a distinct person in accordance with explanation 1 of section 8;

As per Explanation 1 of Section 8:

(i) an establishment of a person in India and any of his establishments outside India, or

(ii)an establishment of a person in a state and any of his other establishments outside that state,

shall be treated as establishments of distinct persons.

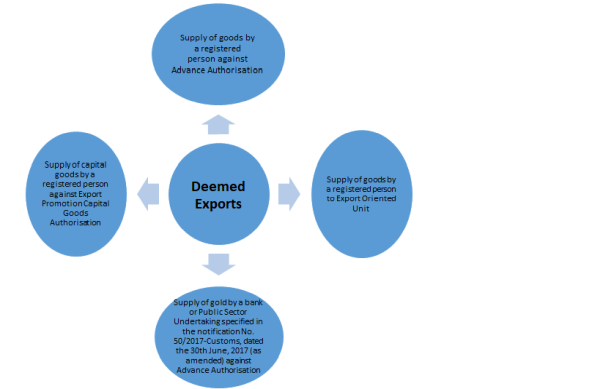

Deemed Exports

Deemed export means the goods supplied, do not leave India and the payment for such supplies is received either in Indian rupees or in convertible foreign exchange, if such goods are manufactured in India.

CAclubindia

CAclubindia