Chartered Accountant

1572 Points

Joined August 2008

What is meant by cancellation of registration?

Cancellation of GST registration simply means that the taxpayer will not be a GST registered person any more. He will not have to pay or collect GST.

Consequences of Cancellation

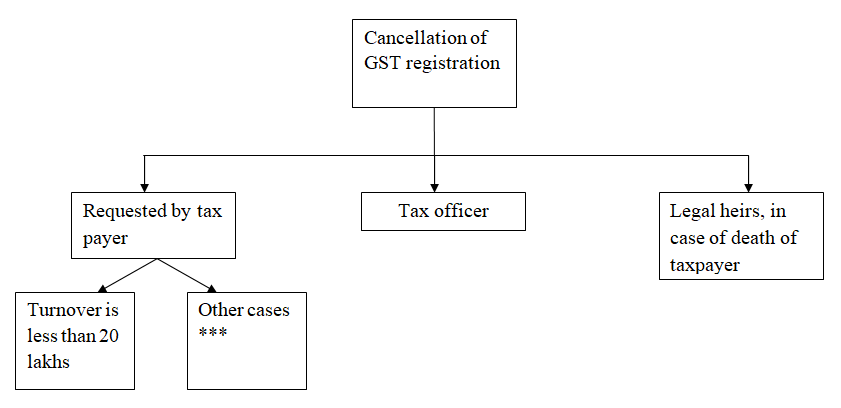

Who can cancel the GST registration?

Cancellation of GST registration can be done by-

*** Application for cancellation, in case of voluntary registrations made under GST, can be made only after one year from the date of registration.

Let us take up each case.

Cancellation when Turnover is less than 20 lakhs

Every person who was registered under old laws had to mandatorily migrate to GST. Many such persons are not liable to be registered under GST.

For example, the threshold under VAT in most states was 5 lakhs whereas it is 20 lakhs under GST. However, do make sure you are not making inter-state supplies since registration is mandatory for inter-state suppliers except for service providers.

Such a taxpayer can submit an application electronically in FORM GST REG-29 at the common portal.

The proper officer shall, after conducting an enquiry as required will cancel the registration.

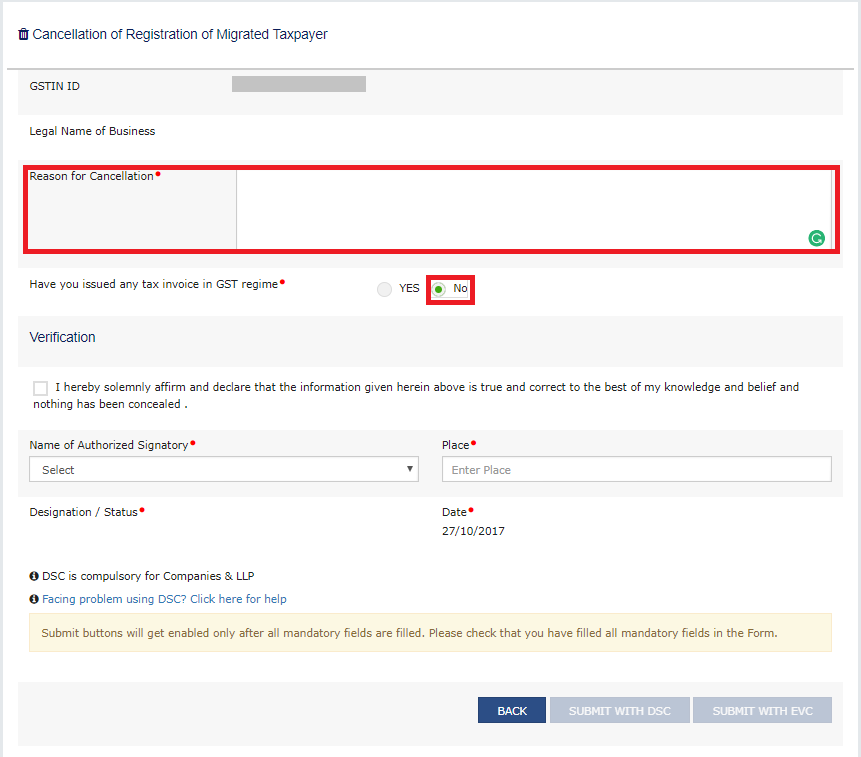

Here are the steps of cancelling on GST Portal-

Step 1

Log in to the GST Portal and click the Cancellation of Provisional Registration

Step 2

- The Cancellation page opens.

- Your GSTIN and name of business will show automatically.

- You are required to give a reason for cancellation.

You will be asked if you have issued any tax invoices during the month.

Simply fill up the details of authorized signatories, place. Finally, sign off with EVC with you are a proprietorship or a partnership. LLPs & Companies must mandatorily sign with DSC.

Note: Taxpayers who have not issued tax invoice can avail above service. If the taxpayer has issued any tax invoice then FORM GST REG-16 needs to be filed.Refer below.

Cancellation by taxpayer in other cases

Get expert assistance to amend your GST registration

Know More

◉ Plans starting from Rs. 999/- ◉ Completely online process

Why does a taxpayer wish to cancel his registration?

- The business has been discontinued

- The business has been transferred fully, amalgamated, demerged or otherwise disposed —The transferee (or the new company from amalgamation/ demerger) has to get registered. The transferor will cancel its registration if it ceases to exist.

- There is a change in the constitution of the business (For example- Private limited company has changed to a public limited company)

Forms for cancellation

All those who cannot follow the above method must file an application for cancellation in FORM GST REG 16. The legal heirs of the deceased taxpayer will follow the same procedure as below.

- Application for cancellation has to be made in FORM GST REG 16.

- The following details must be included in FORM GST REG 16-

- Details of inputs, semi-finished, finished goods held in stock on the date on which cancellation of registration is applied

- Liability thereon

- Details of the payment

- The proper officer has to issue an order for cancellation in FORM GST REG-19 within 30 days from date of application. The cancellation will be effective from a date determined by the officer and he will notify the taxable person

Cancellation by tax officer

Why will the officer cancel registration?

The registration can be cancelled, if the taxpayer-

(a) Does not conduct any business from the declared place of business OR

(b) Issues invoice or bill without supply of goods/services (i.e., in violation of the provisions) OR

(c) Violates the anti-profiteering provisions (for example, not passing on benefit of ITC to customers)

Procedure

- If the proper officer has reasons to cancel the registration of a person then he will send a show cause notice to such person in FORM GST REG-17.

- The person must reply in FORM REG–18 within 7 days from date of service of notice why his registration should not be cancelled.

- If the reply is found to be satisfactory, the proper officer will drop the proceedings and pass an order in FORM GST REG –20.

- If the registration is liable to be cancelled, the proper officer will issue an order in FORM GST REG-19. The order will be sent within 30 days from the date of reply to the show cause.

Revocation of cancellation of registration

What is revocation of cancellation?

Revocation means the official cancellation of a decision or promise. Revocation of cancellation of registration means that the decision to cancel the registration has been reversed and the registration is still valid.

When is revocation of cancellation applicable?

This is applicable only when the tax officer has cancelled the registration of a taxable person on his own motion. Such taxable person can apply to the officer for revocation of cancellation within thirty days from the date of the cancellation order.

Procedure

- A registered person can submit an application for revocation of cancellation, in FORM GST REG-21, if his registration has been cancelled suo moto by the proper officer.

- He must submit it within 30 days from the date of service of the cancellation order at the Common Portal.

- If the proper officer is satisfied he can revoke the cancellation of registration by an order in FORM GST REG-22 within 30 days from the date of receipt of the application. Reasons for revocation of cancellation of registration must be recorded in writing.

- The proper officer can reject the application for revocation by an order in FORM GST REG-05 and communicate the same to the applicant.

- Before rejecting, the proper officer must issue a show cause notice in FORM GST REG–23 for the applicant to show why the application should not be rejected. The applicant must reply in FORM GST REG-24 within 7 working days from the date of the service of notice.

- The proper officer will take decision within 30 days from the date of receipt of clarification from the applicant in FORM GST REG-24.

Note: Application for revocation cannot be filed if the registration has been cancelled because of the failure to file returns. Such returns must be furnished first along with payment of all dues amounts of tax, interest & penalty.

CAclubindia

CAclubindia