hoooooooffffffffff.................hats off to u man....thanks a ton....(and trust me i would love to get an offer from mr. ramalinga raju)

i think m clear at it now......will read it again tomorrow......

thanks to all of u.....

hoooooooffffffffff.................hats off to u man....thanks a ton....(and trust me i would love to get an offer from mr. ramalinga raju)

i think m clear at it now......will read it again tomorrow......

thanks to all of u.....

| Originally posted by : sachin kakkar | ||

|

dnt gt confused just emember if u r an auditor of ho then branch audit wil nt b counted but if u r apointed only for d branch then it will b counted dats it |

|

The answer given by Sachin is short and sweet version of my answer. I gave it in long so as to make you understand the real logic with examples.

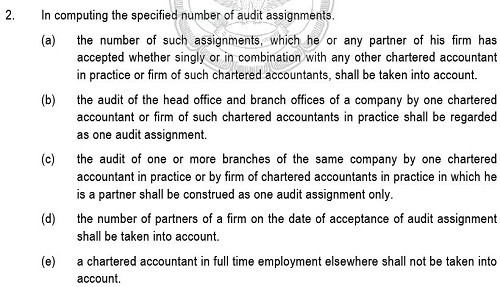

Read point (b) & (c) of above para and visualize difference keeping in mind the background given in earlier replies. There is difference between two points.

Well well well,

Faiz u explained it very well but the view taken by you is horibly wrong. Right now I dont have time to explain you why you are wrong but you better consult some expert on that. I m busy wit studies.

The point is there can be 100 branches and 100 appointment letters. As long as it is for one registered company, the audit limit will be counted as only one. And I am damn sure of that.

Dear Faiz, you have got it wrong(but liked the way you explained it). As I mentioned already, branch audit is not counted for the ceiling u/s 224(1B). The Department of Company Affairs has issued a circular in this respect.

Pls check this link https://www.yourcompanysecretary.com/circulars/S%20224.htm

dear

note the following points

1 if you have the audit of moer than 1 branch of same company than it will be counted only 1 audit for celling.

2 then if you have audit of branch + HO then it also counted only 1 audit.

3 one more thing the if you a audit of branch then it will be counted for your celling as 1 audit,

plz send your valueable feedback.

thanks

abhay

Dear Jithin,

I am thankful to you for providing me the detailed circular on this topic. I was in search of it. I am sorry for my wrong understanding regarding this topic. I was basically thinking on point (b) & (c) given above in scanned material. I was not aware of such circular. The difference between the two points made me to think in a wrong way.

Anyway, I am thankful to you for enlightening me & fellow members.

God bless you.

Thanks.

thanx jitin for the help....

and Faiz ji its perfectly all right...it happens...but u did a lot to explain to me...thanx for that.......never mind...")

phewwww.....I wont forget this clause ever in my life now....lolzzz.....

@ Sneha & Faiz

YOU ARE MOST WELCOME

thanx bhaiya.....

tusi great ho....lolz....

branch audit not considered in counting the limit

As per my opinion and what i had read in my IPCC exams,

Sec 224 1B of The Companies Act deals with the celling numbers of audit assignment an auditor can hold any time during a year. Accordingly an auditor can hold maximum 20 audit assignment out of which not more than 10 companies have a paidup capital of Rs. 25Lacs.

As per your your question what sec 224 1B states that an branch audit shall not be included in counting the audit assignment .

But accoringly an notification issued by ICAI, the max. limit of celling no. of audit assignment are increased from 20 to 30, and while counting the limit of 30 assignment audit of independent branch is to be counted.

Now what an independent branch means???

if an auditor is having audit of branch without HO then it is said to be independent branch. And although the auditor is having the audit of 10 branches of a same company without its HO then also it is to be counted as an single audit assignment

So, overall its means whether an auditor is having the audit of a single independent branch or 10 independent branch of the same company, it is to be counted as a single audit assignment

But if the auditor is having an audit of HO along with its say, 10 branches then it will be counted as only 1 audit assignment (this is the case of dependent branch)

Means audit of independent branches are to be counted as one audit assignment whereas audit of dependent branches are not to be counted for the purpose of celling no. of audit assignment...

Your are not logged in . Please login to post replies

Click here to Login / Register

CAclubindia

CAclubindia

India's largest network for

finance professionals