The Companies Act 2013 mandates Board meetings as an integral part of corporate governance. These are formal meetings of the Directors of a company organized to discuss important topics and problems related thereto. Sections 118, 173, and 174 of the Companies Act, 2013, and Companies (Meetings of Boards and its Powers) Rules, 2014, act as guidelines for conducting board meetings in India.

Board Meeting Notice

As per Section 173(3) of the Companies Act, a board meeting must only be called by giving a notice of not less than 7 days to every director at his address registered with the company, handing them in person, by post, or through electronic mediums.

Note: A meeting of the board may be called on a shorter notice to deal with some urgent business, on the condition that at least one independent director shall be present at the meeting. The decisions shall be circulated and ratified.

Dive deep into Statutory Audit with CA Tushar Makkar and master every aspect with expert insights. Enroll now & level up your audit game!

Penalty for not serving Board Meeting Notice

As per section 173(4) of the Companies Act, 2013 every officer in default to serve notice shall be liable to a penalty of ₹ 25,000.

Adequate Day and Time for Board Meetings

Board meetings may be held on any working day or on a day that is not a public holiday. It can be organized both during business hours and non-business hours.

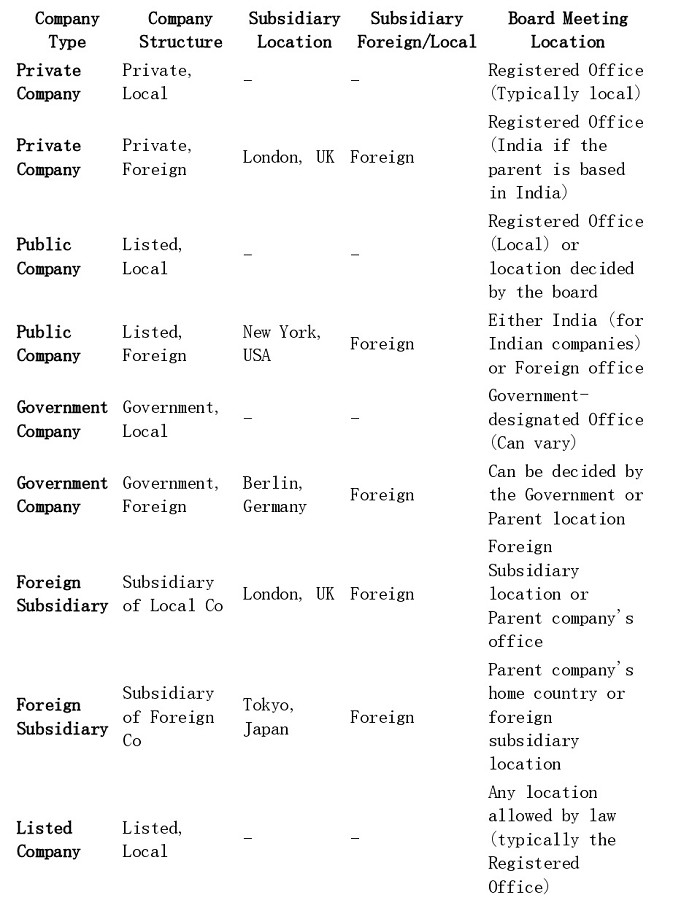

Location for Board Meeting

Board Meeting Quorum

Here's a table that gives an idea about the location for the Board meetings-

The quorum for the meeting of BOD shall be 1/3rd of its total number of directors or 2 whichever is higher.

The Quorum for Section 8 company shall be 8 members or 25% of its total strength, whichever is less.

The participation of directors through video conferencing should also be counted for quorum.

Provision related to Interested Directors

If the number of interested directors exceeds or is equal to two-thirds of the total number of directors, then the non-interested directors, not below the number of 2, shall be the quorum during such time.

Provisions for Adjourned Meeting

Where the meeting of BOD could not be held for the want of quorum then the meeting shall automatically be adjourned to the same day at the same time and place in the next week. But if such day is a national holiday then till the next succeeding day.

Board Meetings for IFSC Companies

International Financial Services Centre Companies are registered in specialized financial zones, allowing them to cater to international clients and businesses.

Specified IFSC private company shall hold its first meeting of BOD within 60 days of its incorporation and thereafter hold at least one meeting of its BOD in each half of a calender year ( Jan-June and July- Dec)

Dive deep into Statutory Audit with CA Tushar Makkar and master every aspect with expert insights. Enroll now & level up your audit game!

Board Meetings for Section 8 Companies

Section 8 companies are non-profit organizations that operate with a focus on promoting arts, science, sports, charity, or any other social cause. Despite their non-profit nature, Section 8 companies are still required to hold general meetings.

Section 8 company shall hold at least one meeting of its BOD within every 6 calendar months.

Gap Between Two Board Meetings

As per Section 173(1), every company shall hold a minimum number of 4 meetings of its board every year in such a manner that not more than 120 days shall intervene between the two consecutive meetings. However, if an OPC, small company, dormant company, or startupprivate company does not default u/s 92, 137 shall be deemedtohave complied with the provisions of this section, if atleast one, meeting of BOD has been conducted in each half of calender year and the gap between the two meetings is not less than 90 days.

CAclubindia

CAclubindia